When you invest in the stock market, your goal is to make a profit. However, it’s important to understand that the profits you make from selling your stocks are subject to taxes-known as capital gains tax. Whether you’re a seasoned investor or just starting out, knowing how and when to pay taxes on your stock market gains is essential for managing your investments effectively.

In this blog, we’ll break down everything you need to know about capital gains tax, including how it works, the tax rates for 2025, and strategies to minimize your tax liability, so you can keep more of your hard-earned profits.

Capital gains tax basics: Taxed on profits from selling assets like stocks or real estate. Rates differ for short-term (10%–37%) and long-term (0%, 15%, or 20%) gains.

Tax rates in 2025: Short-term gains are taxed as ordinary income; long-term gains enjoy lower rates depending on income.

Reducing taxes: Hold assets for over a year for lower rates, or offset gains with losses through tax-loss harvesting.

Filing requirements: Report gains on IRS Form 1040 with Schedule D, and pay taxes quarterly or annually.

Smart planning: Strategic holding and leveraging losses can help minimize taxes owed.

What is the capital gains tax?

Capital gains tax is a tax that you pay on the profit made from selling an asset, such as stocks, bonds, real estate, precious metals & jewelry, for more than what you paid for it. The amount of tax you owe depends on how long you held the asset and your income level.

There are two main types of capital gains:

Short-term capital gains: These are gains from assets held for one year or less. Short-term gains are taxed at the same rate as your ordinary income, which can range from 10% to 37%, depending on your total taxable income.

Long-term capital gains: These are gains from assets held for more than one year. Long-term gains are taxed at a lower rate, typically 0%, 15%, or 20%, depending on your income.

The capital gains tax rate you pay may also vary based on other factors, like the type of asset sold (e.g., real estate or collectibles) or your overall income.

Understanding capital gains tax rates for 2025 is crucial for investors looking to make the most of their profits while managing their tax liabilities. The rate at which you are taxed on your capital gains depends on several factors, including how long you’ve held the asset, your income level, and the type of asset sold. Here’s a breakdown of the capital gains tax rates for 2025:

These brackets apply to long-term capital gains only.

Short-term capital gains are taxed at the ordinary income tax rates for 2025.

For investments subject to Net Investment Income Tax (NIIT), an additional 3.8% tax applies to individuals with modified adjusted gross incomes exceeding $200,000 ($250,000 for married filing jointly).

How to calculate your capital gains taxes?

Calculating your capital gains tax may seem complex, but with the right steps, you can break it down. Here’s a simplified guide on how to calculate the tax you owe on your stock market gain.

1. Determine your asset holding period

Short-term: If you’ve held the asset for one year or less, your gains are considered short-term, and they will be taxed at the same rate as your ordinary income (ranging from 10% to 37%, depending on your total taxable income).

Long-term: If you’ve held the asset for more than one year, your gains are considered long-term and will be taxed at a lower rate, typically 0%, 15%, or 20% depending on your income bracket.

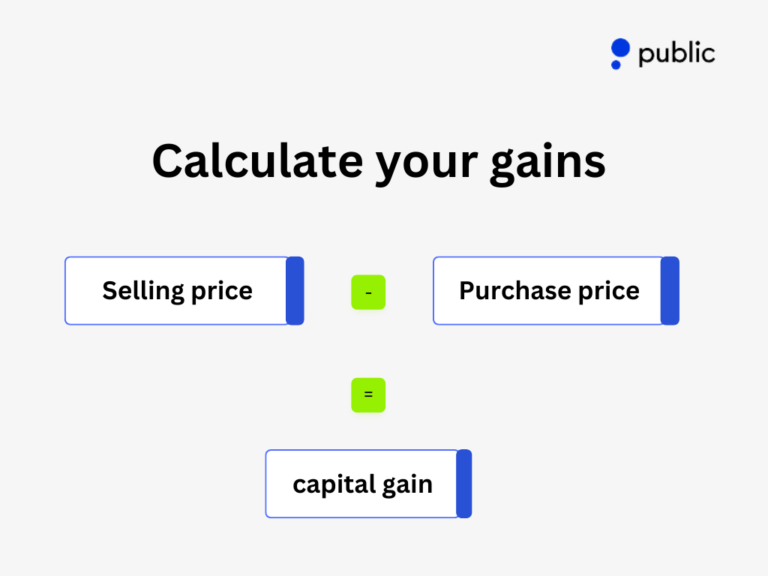

2. Calculate your gains

Subtract the purchase price (what you paid for the asset) from the selling price (what you sold the asset for). The difference is your capital gain.

For example, if you bought 100 shares of a stock at $10 each and sold them for $15 each, your capital gain would be:

If your asset (like stocks) pays dividends, you may need to factor in the dividends you’ve received during the year.

Dividends can be taxable, and in some cases, you may receive qualified dividends, which are taxed at a lower rate than ordinary income.

4. Consider your tax bracket

Short-term gains: Your short-term gains are taxed the same as ordinary income, meaning they will fall under the applicable tax brackets based on your total taxable income. For example, if your total income places you in the 22% tax bracket, your short-term gains will be taxed at 22%.

Long-term gains:Long-term capital gains are taxed based on your income bracket. If you’re in the 0% to 15% bracket, your long-term gains may be taxed at 0% or 15%. If you’re in the highest tax bracket (37%), your long-term gains will be taxed at 20%.

5. Use capital gains tax calculator (Optional)

If you prefer not to do the calculations manually, you can use a capital gains tax calculator to quickly estimate how much you owe. Many online tools, such as those provided by stock brokerages, will ask for details like the type of asset, your holding period, and your income bracket to calculate your capital gains tax.

6. Include any deductions or losses

If you’ve sold an asset at a loss, you may be able to offset those losses against any gains you made. For example, if you had a $500 gain from one stock but a $300 loss from another, you only owe capital gains tax on the $200 net gain.

Capital loss deduction: If your total losses exceed your gains, you may deduct up to $3,000 of net losses from your taxable income per year. You can carry over any remaining losses to future years.

7. File your taxes

You’ll need to report your capital gains on IRS Form 1040, attaching Schedule D to report your capital gains and losses.

Your broker will typically provide a Form 1099-B to report any capital gains or losses from stock transactions.

When to pay taxes on stock gains and other capital gains?

For U.S. investors, taxes on stock and capital gains are due in the year the asset is sold:

Short-term capital gains (held <= 1 year) are taxed at ordinary income rates.

Long-term capital gains (held > 1 year) are taxed at lower rates, ranging from 0% to 20%, depending on your income.

Taxes are reported on your tax return, due by April 15 of the following year. If you expect to owe $1,000 or more, you may need to make quarterly estimated tax payments.

You can offset gains with losses through tax-loss harvesting, reducing taxable income. Keep track of dividends and reinvested gains, as they are also taxable.

Understanding these rules helps you stay compliant and avoid surprises at tax time.

Ways to reduce your capital gains tax burden

Capital gains taxes are something investors must consider when selling assets for a profit. However, there are several strategies you can use to reduce the amount of tax you owe on your gains. Below are some ways to minimize your capital gains tax in 2025:

1. Hold your investments for more than one year

Short-Term vs. long-term gains: If you hold an asset for one year or less, your profits will be taxed as short-term capital gains, which are taxed at ordinary income tax rates (10% to 37%). However, if you hold an asset for more than one year, the profit qualifies as long-term capital gains and is taxed at a lower rate (0%, 15%, or 20%, depending on your income).

2. Offset gains with investment losses

Tax-loss harvesting: You can use your capital losses to offset your capital gains. For example, if you sell an asset at a loss, you can deduct those losses from any gains you’ve made during the year. If your losses exceed your gains, you can deduct up to $3,000 of the excess loss from your taxable income, and any remaining loss can be carried forward to offset future gains.

Example: If you make a $5,000 profit on one investment but incur a $20,000 loss on another, you can use the $5,000 loss to offset your gains. The remaining $15,000 loss can be carried forward and deducted from future taxable income.

3. Utilize tax-advantaged accounts

401(k), IRA, and roth accounts: Certain retirement accounts allow you to buy and sell investments without incurring capital gains taxes. For example, with a 401(k) or IRA, you can trade securities without worrying about paying taxes until you withdraw the funds. With a Roth IRA or Roth 401(k), qualified withdrawals are tax-free after a five-year holding period, which can be a great way to avoid capital gains tax in retirement.

4. Take advantage of capital gains exclusions

Primary residence exclusion: If you sell your primary home, you may qualify to exclude up to $250,000 in capital gains ($500,000 for married couples filing jointly) if certain conditions are met. Be mindful of these rules when planning the timing of your home sale.

5. Consider your timing

Sell in retirement: You may be able to reduce your capital gains tax bill if you wait until you’re retired to sell profitable investments. This is especially beneficial if your income is lower during retirement, as you might fall into a lower tax bracket or even avoid paying capital gains tax altogether.

Watch your holding periods: Make sure that you’ve held an asset for more than a year to qualify for long-term capital gains tax treatment. If you’re close to the one-year mark, waiting a few days to ensure you hit the one-year threshold could save you money.

6. Be mindful of the wash-sale rule

Avoid the wash-sale rule: The IRS disallows tax deductions on losses if you sell a security at a loss and then repurchase the same or a substantially identical security within 30 days. Make sure to avoid this rule if you’re using tax-loss harvesting strategies.

7. Choose the right cost-basis method

FIFO vs. LIFO: When selling securities that were purchased at different times or prices, the method used to calculate the cost basis can affect your capital gains tax. The most common method is first-in, first-out (FIFO), but there are other methods like last-in, first-out (LIFO) or specific share identification. Depending on your specific situation, selecting the most advantageous method may help minimize your capital gains tax.

Record-keeping: Be sure to keep accurate records of your purchases, sales, and associated costs to ensure that you calculate the right cost basis for each asset.

8. Use tax savings tools

Many investors benefit from consulting tax-saving guides or speaking with a tax advisor to make the most of available deductions, exemptions, and credits. Tax laws can be complex, so seeking professional advice can help ensure you take advantage of all available strategies to minimize your tax burden.

By using these strategies, you can lower your capital gains tax liability and potentially increase your overall investment returns. Always consider consulting with a tax professional to optimize your approach to capital gains tax planning.

Bottom line

Managing capital gains taxes is crucial for smart investment decisions. By understanding the differences between short- and long-term gains and using strategies to lower tax liabilities, you can take charge of your finances and optimize returns.

Though taxes might seem complex, tools like online calculators and professional guidance make them manageable. Staying compliant with IRS regulations ensures a stress-free investing journey.

To learn more about personal finance, sign up for the Public App today.