Corporate bonds may offer investors a way to earn interest while lending money to companies. If you’re looking to diversify your portfolio beyond stocks, these fixed-income securities may be worth understanding.

In this guide, you’ll learn what corporate bonds are, the different types available, their potential benefits, and how you can invest in them.

Corporate bonds may offer steady income and higher yields compared to some fixed-income investments.

Different types of corporate bonds include secured, unsecured, investment-grade, high-yield, and convertible bonds, each with varying risk levels and returns.

Factors like credit risk, interest rate fluctuations, and liquidity can impact corporate bond performance, making it important to review ratings and terms.

What are corporate bonds?

Corporate bonds are a type of debt security issued by companies to raise funds for business activities such as expanding operations, financing new projects, or refinancing existing debt. When you purchase a corporate bond, you essentially lend money to the issuing company.

In return, the company agrees to pay you regular interest, known as the coupon rate, until the bond matures. At maturity, the company returns the bond’s face value to you. Corporate bonds can vary widely in terms of risk and return.

They are typically categorized by their credit quality, which is assessed by rating agencies such as Standard & Poor’s, Moody’s, and Fitch Ratings.

Higher-rated bonds (investment grade) may offer lower yields but come with reduced risk, while lower-rated bonds (high-yield or junk bonds) may provide higher yields to compensate for increased risk.

What are the different types of corporate bonds?

Corporate bonds are available in several types, each offering distinct features and risk profiles. Understanding these variations may help you make informed investment decisions:

1. Secured bonds

Secured bonds are backed by company assets, such as real estate, equipment, or other collateral. If the issuer defaults, bondholders may have a claim on the pledged assets. This structure can reduce risk compared to unsecured bonds.

2. Unsecured bonds (debentures)

Unsecured bonds, also called debentures, are not backed by any collateral. Instead, they rely solely on the company’s creditworthiness. If the issuer defaults, you may have to wait behind secured creditors to recover your funds.

3. Investment-grade bonds

These bonds are issued by companies with strong credit ratings (typically BBB- or higher by Standard & Poor’s or Baa3 or higher by Moody’s). They may offer lower yields than riskier bonds, but they tend to have a lower probability of default. If you’re looking for stability, investment-grade bonds may be an option.

4. High-yield (Junk) bonds

High-yield bonds are issued by companies with lower credit ratings (BB+ or lower by S&P or Ba1 or lower by Moody’s). Since these companies pose a higher risk of default, they offer higher interest rates to attract investors. You may consider high-yield bonds if you’re willing to take on more risk for potentially higher returns.

5. Convertible bonds

Convertible bonds provide the option to convert bonds into a specific number of the issuer’s common stock shares. This feature offers potential capital gains if the company’s stock price increases. A real-world example might involve a startup issuing convertible bonds that convert into equity if the company goes public.

Example: How a corporate bond investment works

Let’s say you invest $10,000 in a corporate bond that has:

A 5% annual coupon rate

A 5-year maturity

Interest paid semiannually (which is common for bonds)

Year-by-year breakdown:

Every 6 months, you’ll receive half of the annual interest because payments are semiannual. So, you’ll get:

$250 every six months (since $10,000 × 5% = $500 per year, and $500 ÷ 2 = $250)

This payment is fixed and continues for the entire 5-year period.

Over 5 years:

You’ll receive $500 annually for 5 years, totaling $2,500 in interest income.

These are your coupon payments – regular income for lending your money to the bond issuer.

At maturity (End of year 5):

The company repays your initial investment of $10,000, known as the face value or principal.

Note: This happens as long as the company doesn’t default (i.e., they’re able to meet their debt obligations).

Total return summary:

Total interest earned: $2,500 (across 10 semiannual payments of $250)

Principal repaid: $10,000

Total received over 5 years: $12,500

Why corporations may choose to issue bonds?

Corporations may issue bonds for several strategic reasons, including:

Raising capital for growth: Bonds can help fund expansion, acquisitions, or research and development without diluting shareholders’ equity.

Refinancing existing debt: Companies may issue new bonds to replace old ones, potentially securing more favorable terms.

Managing cash flow: Bonds can provide a stable source of funding for ongoing operations or specific projects.

What happens if bond issuer company declares bankruptcy?

If a company files for bankruptcy, the repayment hierarchy determines how much you, as a bondholder, may recover:

Secured bondholders: If you hold secured bonds, you may have the first claim on specific company assets, which could improve your chances of recovering funds.

Unsecured bondholders: If your bonds are unsecured, you may only receive payments after secured creditors have been paid, which could mean a partial repayment.

Subordinated bondholders: If you own subordinated bonds, you may be among the last creditors to be repaid, which means you could recover little or nothing.

Equity shareholders: If you own company shares, you may only receive a payout if all bondholders and creditors have been repaid—something that rarely happens in bankruptcy cases.

Benefits of investing in corporate bonds

Corporate bonds may offer a balanced mix of income, stability, and diversification for investors.

1. Steady income stream

One of the key reasons you might invest in corporate bonds is the regular interest payments they provide. These payments can help generate a steady income stream, which may be useful if you’re planning for retirement or need a consistent cash flow.

2. Portfolio diversification

If you already invest in stocks, adding corporate bonds to your portfolio may help spread risk. Bonds tend to react differently to market conditions than stocks, which may help stabilize your overall investment returns, although diversification is not a guarantee against loss.

3. Capital preservation (Depending on the bond type)

Certain corporate bonds, especially investment-grade ones, may offer a level of capital preservation. As long as the issuer does not default, you will receive your original investment back at maturity.

4. Variety of choices

With thousands of corporate bonds available, you may find options that match your preferred risk level, industry exposure, or return potential. Whether you seek lower-risk investment-grade bonds or higher-yield bonds with greater risk, the bond market may offer flexibility.

Potential risks to consider before investing in corporate bonds

While corporate bonds may offer potential benefits, they might also come with certain risks that investors should evaluate before making a decision.

1. Credit risk (Default risk)

If the issuing company faces financial difficulties, it may struggle to pay interest or repay your principal at maturity. Bonds from lower-rated companies may carry a higher chance of default, making them riskier investments.

2. Interest rate risk

When interest rates rise, the price of existing bonds typically falls as new bonds with higher yields become more attractive. This means if you need to sell your bond before maturity, you might receive less than what you originally paid.

3. Inflation risk

Since corporate bonds provide fixed interest payments, rising inflation can reduce the purchasing power of your returns. Over time, the real value of both your interest earnings and principal repayment may decline.

4. Liquidity risk

Some corporate bonds, especially those issued by smaller companies, may not have a large market of buyers. This can make it difficult to sell your bond quickly at a fair price if you need to exit your investment early.

How do you buy corporate bonds on Public.com?

Investing in corporate bonds on Public.com is a simple process that allows you to access whole and fractional bonds with ease.

1. Sign up for a brokerage account on Public

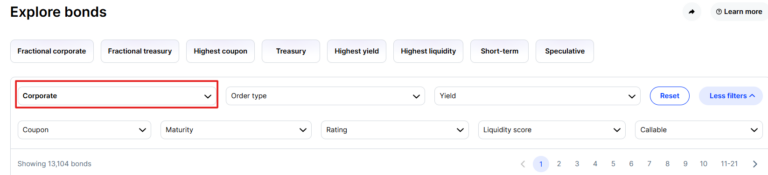

You can sign up for an account and explore thousands of corporate bonds on our bonds screener tool from the Trade tab.

2. Add funds to your Public account

Fund your Public account by linking a bank account or by depositing with a debit card.

3. Purchase whole or fractional bonds

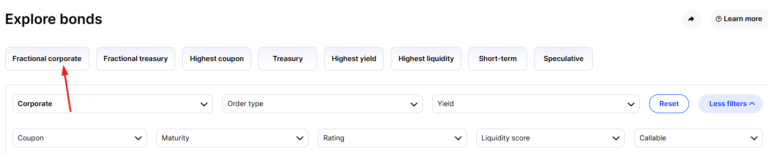

On Public, you can purchase fractional bonds for as little as $100. Just look for the “Fractional” tag.

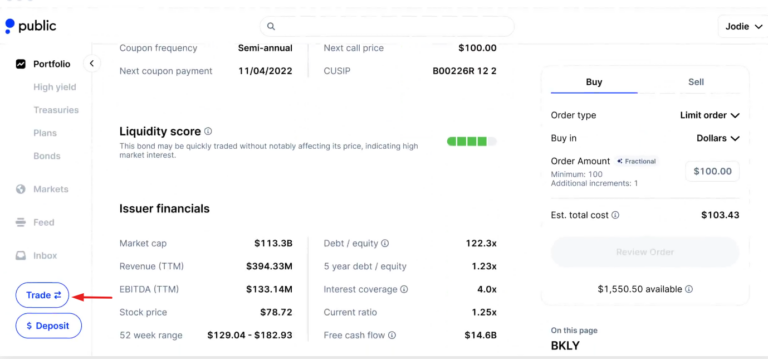

4. Complete your corporate bond purchase in a few taps

Once you’ve selected your bond, hit the “Trade” button to complete your purchase. If it’s a fractional bond, you can enter any dollar amount.

5. Manage your investments in one place

You can find your newly purchased corporate bonds in your portfolio alongside the rest of your stocks, options, crypto, U.S. treasuries, IRAs and other assets.

Conclusion

Corporate bonds may provide a source of income and portfolio diversification, but they also come with risks, including credit risk, interest rate risk, and inflation risk. If you’re considering investing in corporate bonds, reviewing their credit ratings, maturity dates, and interest rates may help you make informed decisions.

If you’re looking to invest in corporate bonds, Public.com provides a simple and seamless way. With a Public Bond Account you can invest in a diversified set of bonds with every deposit. It’s a new way to invest in corporate bonds designed for a more streamlined experience.

Open a Public Bond Account today and take the next step toward building your fixed-income portfolio.

FAQs

How is investing in U.S. Treasury bonds different from investing in corporate bonds?

U.S. Treasury bonds are issued by the federal government and are considered lower risk because they are backed by the U.S. government. Corporate bonds, on the other hand, are issued by companies and carry a higher risk of default but may offer higher interest rates.

Are corporate bonds safe?

Corporate bonds carry varying levels of risk depending on the issuer’s credit rating. Investment-grade bonds from financially strong companies may be generally considered lower risk, while high-yield (junk) bonds may have a higher risk of default.

How are corporate bonds taxed?

Interest income from corporate bonds is generally taxed as ordinary income at your federal, in most cases, state, and local taxes. You may also owe capital gains tax if you sell a bond before maturity at a profit.